For Sellers:

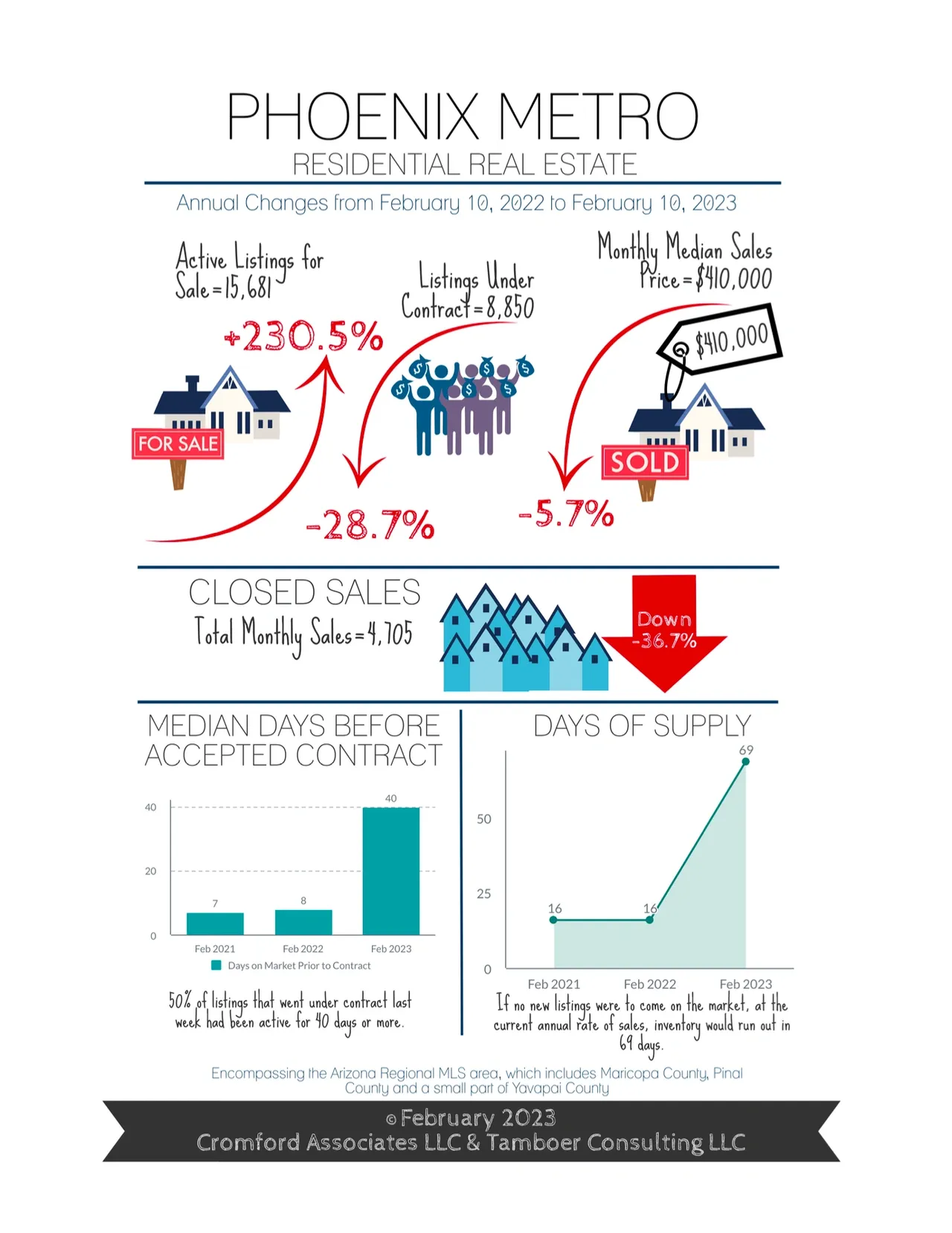

Don’t be fooled by this seller’s market, it is nothing like the seller’s market of early 2022. Sellers may notice there is less pressure for a price reduction as there are few new listings entering the market. There were only 9,664 new listings add- ed to the Arizona Regional MLS since the beginning of 2023, the lowest number of new listings measured in at least 23 years. The median is 14,000 listings, and the highest measured was over 21,000 in 2006 over the same 5-week time frame. Less competition is good for price stability.

Sellers may notice fewer days on market prior to contract. Half of owners who accepted contracts last week were on the market for 40 days or less (listed after January 4th) compared to the peak of 56 days in December. In a weak seller’s market like this, as we shift into the Spring season, days on market prior to contract may settle in at 25-30 days; a far cry from the 5-7 days in early 2022.

Sellers will notice little change in negotiations or concessions at this stage. Last month, 51% of sales involved seller con- cessions to the buyer with a median cost of $9,700. So far in February, 47% have involved concessions at a cost of $9,800. The average negotiation is 2.8% below the last list price, down from 3.5% last month. Sales measures rolling in now are reflecting contracts written in late December and early January, which was a mixed bag of cities in balance and cities in buyer’s markets at the time. The effects of the current seller’s market will not be seen in sales price measures until March, at which point we expect to see the rate of decline in sales price measures either slow down or stabilize. Mortgage rates could change the game quickly, however. It’s not a time for buyers or sellers to take market conditions for granted.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report ©2023 Cromford Associates LLC and Tamboer Consulting LLC.